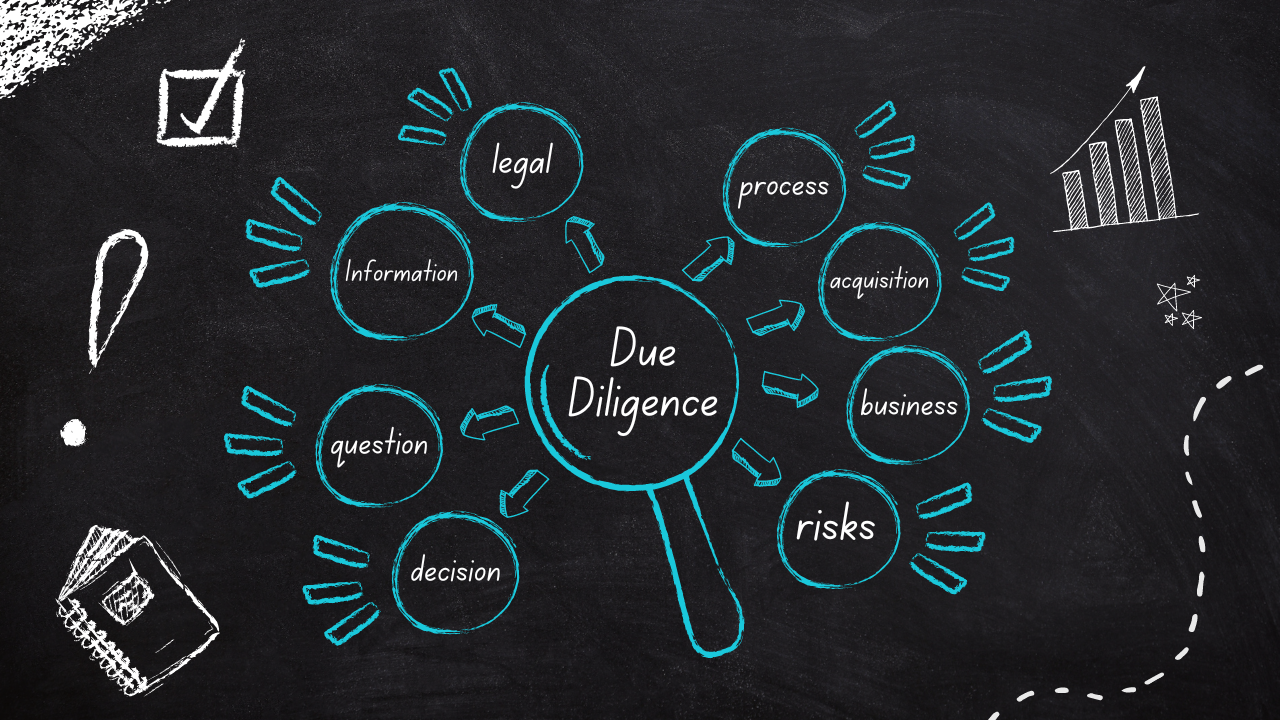

A Due Diligence Deep Dive

If you’re someone who hated homework in high school - we’ve got some bad news for you.

The expression “what you don’t know can’t hurt you” might be valid for a lot of things, but when it comes to buying a business, what you don’t know is precisely what could bite you in the ass.

Performing due diligence is one of the most critical steps when purchasing a business. I don’t care if the dude you’re buying from is your brother’s best friend’s sister’s step-uncle, who you’ve known since you were in diapers. You should always, ALWAYS, do your homework before making anything official. A misrepresentation of facts or figures - intentional or otherwise - is always a possibility. Protect yourself from agreeing to a crap deal. Remember, it's not personal - it’s business.

When is it done?

Due diligence is typically one of the final phases of your business acquisition journey. You’ve already scoped out what you want to buy, spoken with the owner, made an offer, and negotiated the price and ...

The ABC's of Small Business

Your business is in a constant state of evolution. Workflows can be improved; sales increased; processes honed; client experiences enhanced. Vertically. Horizontally. Improvement is a continuous pursuit.

The history of the Oxford English Dictionary is an ideal example of this mindset. Googling a word’s meaning or – gulp – leafing through an actual paperbound dictionary is somewhat of a luxury. When the Philological Society of London members decided, in 1857, that existing English language dictionaries were incomplete and deficient, they called for a complete re-examination of the language. While they knew they were embarking on an ambitious project, they didn’t realize the full extent of the work they initiated or how long it would take to achieve the final result.

The project proceeded slowly after the Society’s first grand statement of purpose. Eventually, in 1879, the Society agreed with the Oxford University Press and James A. H. Murray to begin work on a New English Dictionary...

A Tale of Two E's: Entrepreneurship and Ego

Entrepreneurs must have an ego. As at the bar during happy hour, everything in moderation, kids!

There are tons of reasons companies (big and small) fail, but it often comes down to one thing: hubris. Their leaders lack humility. Oddly, this lack of humility in the pursuit of largesse keeps them from realizing just what an enormous problem that is. It keeps them in denial of their own limitations.

There is no better example of this folly than a successful company deciding to build a new home for their operations - only to have their businesses collapse soon after that under the weight of excessive costs and overhead.

These case studies are not here because we like lists. They're offered to you because the good ones learn from their mistakes. The great ones learn from the mistakes of others. Be great.

At the height of print media and ignoring the heavy footsteps of the internet, The New York Times Company built a 52-floor monolith as the business' client base was being taken away from it....

5 Unexpected Costs of Operating a Business

"By failing to prepare, you are preparing to fail."

Unexpected costs when running a business are going to pop up at the worst possible time (think giant zit right before the big high school dance kind of timing). It doesn't matter how carefully and thoroughly you planned your budget – Murphy's Law guarantees the one expense you didn't account for is the one you're going to incur.

With that in mind, today, we're going to cover five unexpected costs you might encounter as a business owner. It's our way of giving you the upper hand…and giving ole Murphy the middle digit.

Equipment Failure & Maintenance

Nothing lasts forever, and at some point, everything from construction equipment, machinery, ovens, printers, and computers will need servicing or replaced altogether. Depending on the nature of your business, some of these will immediately negatively impact your bottom line. (If you have a print shop and your printers go up, you're in trouble.)

Consider This: What equipment is vita...

7 Ways to Increase Brand Awareness

Picture it. You have a swell idea or product that could turn the world on its head and put a stop to climate change, end world hunger, and bring peace to the Middle East. Where do we sign?

Don’t start writing your Nobel Peace Prize acceptance speech quite yet, friend. Because at the end of the day, it doesn’t matter how good the idea is if nobody knows (or cares) about it.

Enter Brand Awareness.

What is it?

Brand awareness is simply what makes people aware of your very existence and helps set you apart from your competitors. It’s your opportunity to present your products or services in such a way that makes them easily recognizable to customers, as well as establish your authority or expertise.

Why is it important?

It establishes trust with your customers and influences their decision-making processes. The better brand awareness you have, the more valuable your business is. Cha-ching! When you think of dish soap or sneakers or search engines, are you thinking of these in ...

Attracting More Customers, Finding Good Employees, and Improving Your Customer Relation Skills

All businesses have many moving parts and pieces that contribute to or detract from their overall success. Profit margins, supply chain and inventory issues, customer relations, inflation, funding, cash flow, and competition are just the tip of the iceberg.

If you don't want to sail a sinking ship, you need to keep your ear to the ground (or deck, maybe?) on each and every one of these. But for today, we're going to focus on three areas that are all interconnected and can significantly impact your business -- for good or for bad.

Finding Customers.

Recruiting and Retaining Dedicated Employees.

Developing Good Customer Service.

- For a business to grow, you need to attract more customers.

- More customers mean you need to hire more employees to keep up with the demand.

- More demand means more employee and customer interactions.

- More interactions mean more opportunities for employees to provide excellent (or not so excellent) customer service.

- Excellent customer service means...

Avoiding Entrepreneur Burnout

Burnout: exhaustion of physical or emotional strength or motivation usually as a result of prolonged stress or frustration (Merriam-Webster Dictionary)

If you're an entrepreneur or small business owner, you probably don't need the dictionary definition of the word; it's a reality you're all too familiar with. Starting a business -- and keeping it operational -- is no small feat. Elon Musk describes it as "eating glass and staring into the abyss. If you go into expecting that it's going to be just fun, you're going to be disappointed. It's not. It's quite painful."

Cheery, right?

So, why do people do it? What makes entrepreneurs take the long, hard path with no shortcuts and no guaranteed success? Why the hell would someone choose to take "the road less traveled" when there are plenty of other safer, less tumultuous options out there? I know Robert Frost claimed it made all the difference, but to what end?

Because you want something more. Because you don't want to settle. Because y...

How to be a Better Decision Maker

If your decision-making skills closely resemble a squirrel trying to cross the street, keep reading.

As a small business owner, you are confronted daily with (what feels like) thousand-and-one decisions -- many of which you don't even realize you're making. But even though you're getting a ton of practice, there is always room for improvement. Effective decision-making is one of the most powerful tools business owners have to drive action; cultivating this skill should not be overlooked.

The process of decision-making falls into two broad categories: Intuitive and Rational. Intuitive decisions rely on a "sixth sense" or "gut feeling." They tend to be more emotional-based and influenced by a person's mood. These types of decision-makers are looking for an outcome that feels right. Meanwhile, rational decisions are based on data and facts. It's a more black-and-white approach that has little regard for the emotional consequences and prioritizes an outcome that makes sense.

Neither...

How to Bring More Value to Your Business

"When you stop growing you start dying."

This cheerful little quip (credited initially to William S. Burroughs) is a poignant reminder for small business owners that becoming stagnant isn't an option if you want to be successful. And that's the goal, right? If you want to create long-term success - not to mention survive the competition - you can't rest on your laurels or settle for the status quo. You need to be proactive.

One of the ways you can do this is by increasing the value of your business. This can lead to better profit margins, happier employees, more satisfied customers, and scalability - which means you can continue operating for years to come (or at least as long as you'd like).

You can add value to your business in various ways, some of which are entirely free while others require a bit more time or money. Below we've listed seven areas you can focus on today to get started.

Review the Current SOPs

Standard Operating Procedures (SOPs), when done well, are detail...

7 Common Mistakes to Avoid When Buying a Business

Owning a business is a dream for many. And by purchasing one that’s already up and running, you avoid the headaches, stress, and risk of starting one from scratch. It’s sort of like adopting a teenager instead of a newborn. You already have a pretty good idea of what you’re getting into.

But like teenagers, there’s an element of the unexpected and still plenty of mistakes you can make. To help you navigate this new territory, here are 7 Common Mistakes to Avoid When Buying a Business.

Mistake #1: Not understanding why the business is for sale.

Seller motivation is always one of the first things you should look into. There are plenty of legit reasons why someone would want to sell their business. They might be planning a cross-country move, want to explore a new industry, or are simply ready to retire. It could also be because it’s hemorrhaging money, they’re having trouble retaining employees, the production costs are too high, and so on. You might not discover their true motiv...

Like what you see?

Subscribe to The Weekly to receive actionable advice and “outside of the box” ideas for all things business from Shield Advisory Group.

Surround Yourself With 1000's of Like- Minded Business Owners and Leading Experts.

Recent Posts

Categories

All Categories